Fill a Valid Sf 16 Georgia Template

Fill a Valid Sf 16 Georgia Template

Incorrectly Calculating Acquisition Costs: Many individuals fail to accurately compute the total acquisition cost. This includes not adding all relevant expenses such as the sales price, land cost, and any construction interest.

Excluding Necessary Documentation: Some applicants neglect to attach required documents, such as appraisals or contracts, which can lead to delays or rejections.

Misunderstanding Fixture Definitions: A common mistake involves confusing personal property with fixtures. Items like refrigerators or stoves must be correctly categorized to avoid misrepresentation of the acquisition cost.

Omitting Subtractions: Applicants often forget to subtract personal property values or services provided by family members, which can distort the final acquisition cost.

Failing to Sign and Date: Incomplete forms frequently result from missing signatures or dates, which can invalidate the submission.

Ignoring the Two-Year Rule: Some borrowers mistakenly include land owned for more than two years in their calculations, which is not required according to the guidelines.

What is the purpose of the SF 16 Georgia form?

The SF 16 Georgia form is used for the Georgia Dream Homeownership Program. It serves as an Acquisition Cost Certification that must be submitted with the purchase package for the Georgia Dream First Mortgage Program. This form helps to calculate the total acquisition cost of the property, including the purchase price, land costs, and other necessary expenses related to the home. Accurate completion of this form is essential for determining eligibility for the program.

Who needs to fill out the SF 16 form?

The SF 16 form must be filled out by the borrower and the property seller involved in the transaction. The borrower is typically the individual or individuals seeking to purchase the home, while the property seller is the current owner of the residence. Both parties must provide accurate information regarding the sale and any associated costs to ensure compliance with the requirements of the Georgia Dream Homeownership Program.

What information is required on the SF 16 form?

The form requires detailed information about the acquisition cost of the land and dwelling. Borrowers must provide the sales price, costs of land, appraised values, interest paid during construction, and other related expenses. Additionally, any subtractions, such as personal property items and the value of services performed by family members, must be included. This comprehensive data is crucial for calculating the total acquisition cost, which influences eligibility for the mortgage program.

What happens if the information provided on the SF 16 form is incorrect?

Providing incorrect information on the SF 16 form can lead to serious consequences, including the potential denial of the mortgage application. Misrepresentation may also result in legal penalties, as the borrower declares under penalty of perjury that the information is true and correct. It is important to ensure that all details are accurate and complete to avoid any issues with the Georgia Department of Community Affairs and to maintain eligibility for the program.

G-7 Return - Payments can include checks or money orders as outlined in the G-7.

In addition to its significance in private transactions, obtaining a Georgia Bill of Sale form can also be easily facilitated through resources available online, such as OnlineLawDocs.com, which offers comprehensive templates and guidelines for ensuring a smooth transfer of ownership.

How to Change Last Name in Georgia After Marriage - Verify that both parents' consents are present unless there's sufficient rationale for lack thereof.

Georgia Net Worth Tax - Clean recordkeeping practices enhance the integrity of the funeral service provider.

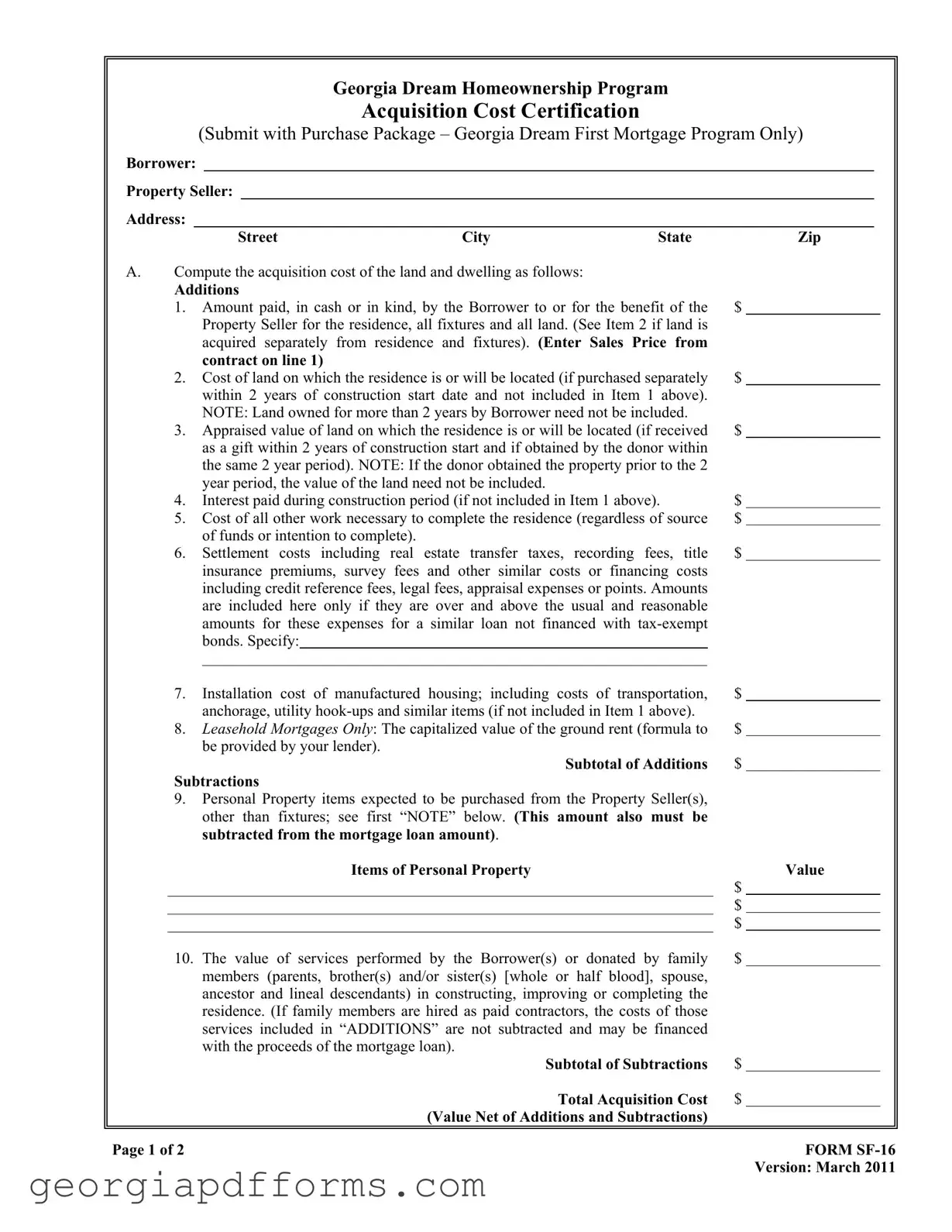

Georgia Dream Homeownership Program

Acquisition Cost Certification

(Submit with Purchase Package – Georgia Dream First Mortgage Program Only)

Borrower:

Property Seller:

Address:

Street |

City |

State |

Zip |

A.Compute the acquisition cost of the land and dwelling as follows:

Additions |

|

|

1. |

Amount paid, in cash or in kind, by the Borrower to or for the benefit of the |

$ |

|

Property Seller for the residence, all fixtures and all land. (See Item 2 if land is |

|

|

acquired separately from residence and fixtures). (Enter Sales Price from |

|

|

contract on line 1) |

|

2. |

Cost of land on which the residence is or will be located (if purchased separately |

$ |

|

within 2 years of construction start date and not included in Item 1 above). |

|

|

NOTE: Land owned for more than 2 years by Borrower need not be included. |

|

3. |

Appraised value of land on which the residence is or will be located (if received |

$ |

|

as a gift within 2 years of construction start and if obtained by the donor within |

|

|

the same 2 year period). NOTE: If the donor obtained the property prior to the 2 |

|

|

year period, the value of the land need not be included. |

|

4. |

Interest paid during construction period (if not included in Item 1 above). |

$ |

5. |

Cost of all other work necessary to complete the residence (regardless of source |

$ |

|

of funds or intention to complete). |

|

6. |

Settlement costs including real estate transfer taxes, recording fees, title |

$ |

|

insurance premiums, survey fees and other similar costs or financing costs |

|

including credit reference fees, legal fees, appraisal expenses or points. Amounts are included here only if they are over and above the usual and reasonable amounts for these expenses for a similar loan not financed with

7. |

Installation cost of manufactured housing; including costs of transportation, |

$ |

|

anchorage, utility |

|

8. |

Leasehold Mortgages Only: The capitalized value of the ground rent (formula to |

$ |

|

be provided by your lender). |

|

|

Subtotal of Additions |

$ |

Subtractions

9.Personal Property items expected to be purchased from the Property Seller(s), other than fixtures; see first “NOTE” below. (This amount also must be subtracted from the mortgage loan amount).

Items of Personal Property

$

$

$

Value

|

10. The value of services performed by the Borrower(s) or donated by family |

$ |

|

|

|

|

members (parents, brother(s) and/or sister(s) [whole or half blood], spouse, |

|

|

|

|

|

ancestor and lineal descendants) in constructing, improving or completing the |

|

|

|

|

|

residence. (If family members are hired as paid contractors, the costs of those |

|

|

|

|

|

services included in “ADDITIONS” are not subtracted and may be financed |

|

|

|

|

|

with the proceeds of the mortgage loan). |

|

|

|

|

|

Subtotal of Subtractions |

$ |

|

|

|

|

Total Acquisition Cost |

$ |

|

|

|

|

(Value Net of Additions and Subtractions) |

|

|

|

|

|

|

|

|

||

|

Page 1 of 2 |

|

FORM |

||

|

|

|

Version: March 2011 |

||

NOTE: A “fixture” is property that is affixed to real estate, which the Borrower(s) intend(s) (i): to keep so affixed during its useful life, and (ii) to be part of the real estate. Refrigerators,

NOTE: The acquisition cost of a Single Family Dwelling does not include:

(1)Usual and reasonable settlement and financing costs; “Settlement Costs” include titling and transfer costs, title insurance, survey fees and other similar costs; and “Financing Costs” include credit reference fees, legal fees, appraisal expenses, points which are paid by the Borrower, or other costs of financing the residence. Such amounts must not exceed the usual and reasonable costs which otherwise would be paid for in a similar loan,

(2)The imputed value of services performed by the Borrower or members of his family (which include only the Borrower’s parents, brother(s) and/or sister(s) [whether by whole or half blood], spouse, ancestors and lineal descendant(s) in constructing or completing the residence, or

(3)The cost of land which has been owned by the Borrower for at least 2 years before the date on which the construction of the structure comprising the Single Family Residence begins.

B.To the best of our knowledge, all of the land sold with this residence reasonably maintains the basic livability of the residence.

I fully understand the information set forth above is material to the Georgia Department of Community Affairs and declare under penalty of perjury, which is a felony offense in the State of Georgia that the above information is true and correct.

Subject Property Address: ________________________________________________________________

__________________________________________________________________ , Georgia

Borrower’s Signature |

|

Date |

|

|

|

|

Date |

|

|

|

|

Property Seller’s Signature |

|

Date |

|

|

|

Property Seller’s Signature |

|

Date |

I further certify that the real estate on which the home is located does not provide a source of income to the borrower.

______________________________________________________ |

________________________________ |

Borrower’s Signature |

Date |

______________________________________________________ |

________________________________ |

Co Borrower’s Signature |

Date |

Page 2 of 2 |

FORM |

|

Version: March 2011 |

When filling out the SF 16 Georgia form for the Georgia Dream Homeownership Program, keep these key takeaways in mind:

| Fact Name | Details |

|---|---|

| Purpose | The SF-16 form is used for the Georgia Dream Homeownership Program to certify acquisition costs when applying for a first mortgage. |

| Components | The form requires borrowers to detail costs related to the land, dwelling, and additional expenses, while also allowing for certain subtractions. |

| Exclusions | Costs that are not included in the acquisition cost calculation include usual settlement and financing costs, and the value of services performed by family members. |

| Governing Law | This form is governed by the Georgia Department of Community Affairs regulations and applicable state laws regarding homeownership assistance. |